That’s the title of a new paper co-authored with Ahmad Wahdat, in which we attempt to quantify potential vulnerabilities of different food processing sectors to disruptions in the upstream input supplies.

Here is the abstract:

“The modern day food industries are part of a complex agri-food supply chain, where food production has become efficient, yet potentially vulnerable to supply chain risks. The COVID-19 pandemic is a testament to that end. This article measures and identifies the U.S. food manufacturing industries’ vulnerability to upstream industries and labor occupations by (i) calculating a food industry’s diversification of intermediate input purchases across upstream industries, (ii) quantifying the relative exposure of food manufacturing in a given industry and location to upstream input suppliers and labor occupations, and (iii) estimating each food industry’s gross output elasticity of inputs. Among our results, we find the evidence that the animal processing industry’s output is relatively vulnerable to production labor which is consistent with the observed disruptions to the meat packing sector during COVID19, which were largely caused by labor issues. Our results may help academics and practitioners to understand food industries’ vulnerabilities to upstream industries and labor occupations.”

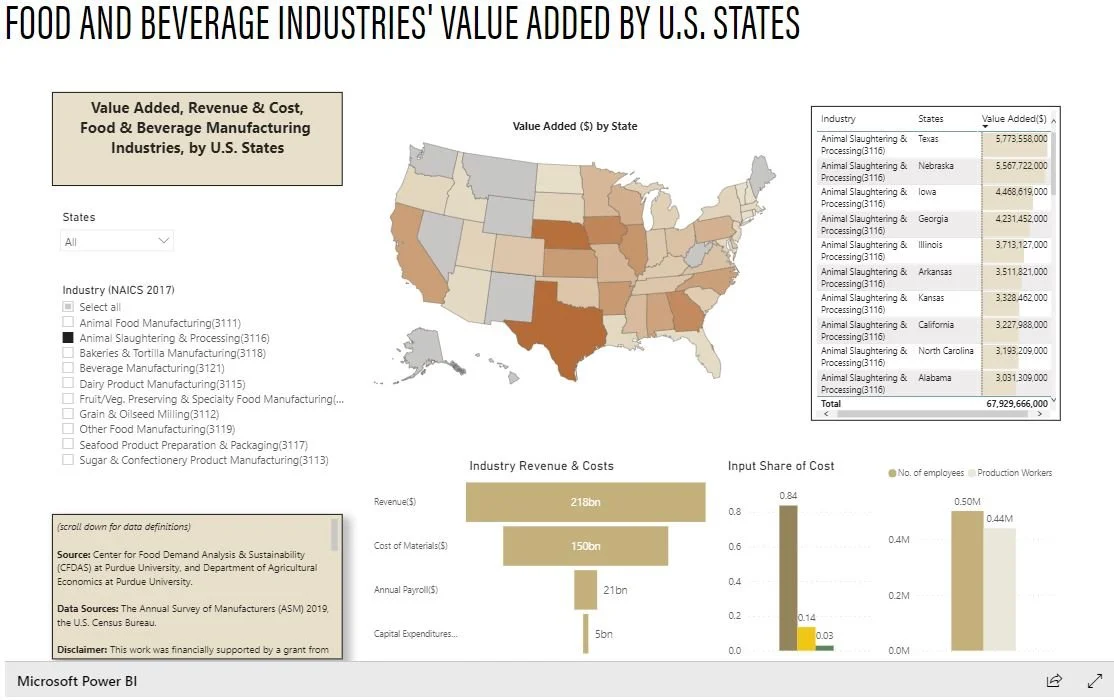

The approach also allows us to explore geographic differences in a food processing sector’s concentration of input purchases, as shown for example, in the charts below for the oilseed milling industry.