The journal Applied Economic Perspectives and Policy just accepted a paper I've written with Glynn Tonsor, which provides new estimates of consumer demand for different meat products using what is probably one of the largest and longest-running surveys choice experiments (a survey method) to date.

The graph below showing changes in retail meat prices from January 2010 to January 2015 is what motivated the paper. Beef and pork prices rose dramatically over this period (note: in the past few months they've come back down) whereas chicken prices were and still are fairly stable. The following is further motivation from the paper:

“Industry observers have expressed surprise about how consumers have responded to recent price changes (Ishmael, 2014). In particular, expenditures for beef and pork have not fallen as much as some people expected given the high prices. Industry analysts have asked “where is the tipping point” when consumers will stop buying beef and pork (Rutherford, 2014), but it may be that demand elasticities are more non-linear than previously realized. Moreover, relative price swings would have seemed to have favored chicken over beef and pork, and yet there does not seem to be a high degree of substitution in the current market environment. Such observations raise the possibility that cross-price elasticities have changed or are lower at higher price levels.”

You can read the paper for the methods. Here I'll just highlight what we found.

First, people with different incomes choose different things. High income consumers are more likely to choose steak and chicken breast than are low income consumers, and the opposite is the case for chicken wings, ground beef, and deli ham.

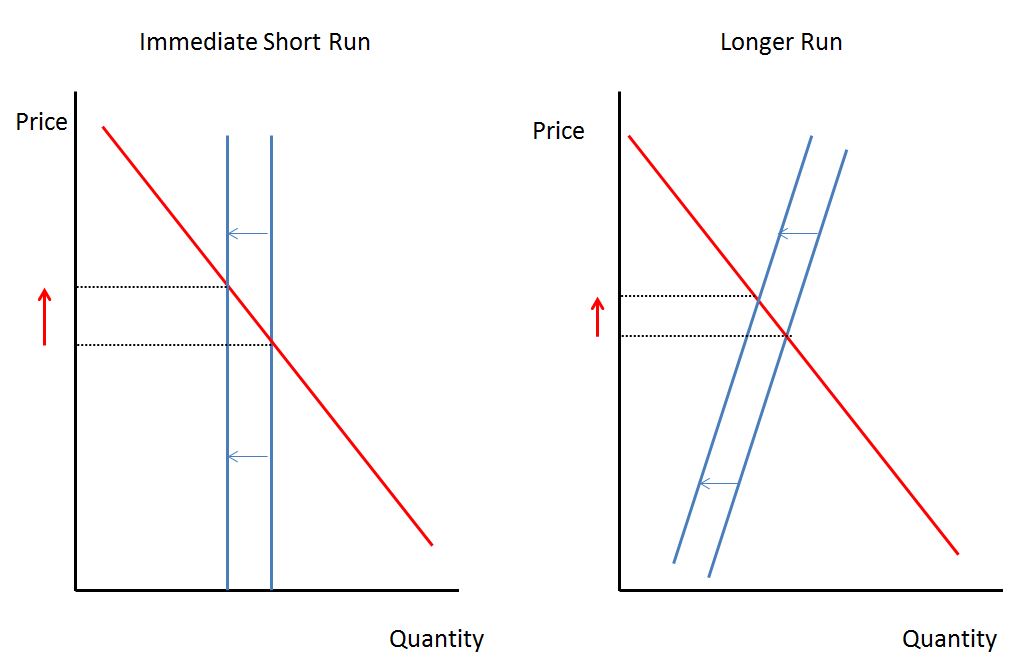

Second, beef prices are more sensitive to changes in the price of chicken than the reverse. Here's an illustration of that phenomenon using our estimated model for middle income consumers.

Third, and somewhat surprisingly (though consistent with industry observations over this period), the quantity of beef and pork demanded is less sensitive to price changes when prices are high as compared to when prices are low. In econ-jargon, demand is more inelastic as prices rise. You can see that in the graphs above, and the paper fleshes out that finding a bit more by showing the bias in models that ignore this non-linearity in demand.

Hopefully these new estimates will help us better predict in the near future what happens when beef and pork prices fall, and will help producers better anticipate the impacts of future price hikes.

This analysis used a huge data set (110,295 choices made by 12,255 consumers) collected over a year and half long period. This is of course from my Food Demand Survey (FooDS). The present analysis assumed people's preferences staid the same over this period. Up next on the research agenda is to look at how these demand estimates have been changing (or not) over time using even more data over a longer time period., and investigating whether these survey-based demand changes can forecast changes in retail meat prices.