In the Food Police, I wrote the following about local foods when critiquing the argument that a larger local food system would be better for the environment and for food security:

“Because of common weather and temperature, all farms within a region are likely to have their produce come to market around the same time. In a world with regional and international trade, that isn’t a big deal as the surplus can be shipped out to other locations. But, in the locavore’s world, the result is inevitable: spoilage and waste.

...

It would be foolish to invest all your retirement savings in a single stock. The financial experts tell us to diversify. And if we shouldn’t keep all our financial eggs in one basket, the same goes for the real ones. One of the things that makes farming unique compared to other businesses is its unusually large reliance on the weather. An unexpected drought, a rain at the wrong time, an early freeze, or a hail storm can devastate a whole farming community or even an entire region. While farmers protect themselves financially against these kinds of risk by buying crop insurance, what about the food consumer? ”

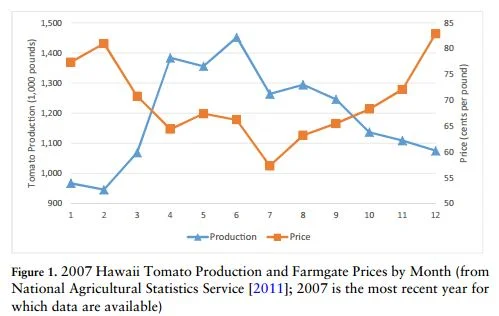

This new paper in the Journal of Agriculture and Applied Economics by some Hawaiian researchers provides some empirical evidence of the price volatility I mention surrounding local foods. Here's a graph from their paper showing production and prices of local tomatoes over 12 months of the year

There is a very clear negative correlation between production and price. When tomatoes are "in season" and local producers have a lot to sell, prices are low, and vice versa.

Of course, that inverse relationship is true for most of agricultural production. But, here's the difference for a lot of local food production: A) with grains you can store the commodity to help smooth out prices over time (something much harder with perishable fruits and vegetables) and B) with trade you can ship to locations with different seasons (where there is less supply and therefore higher prices).

In short, by limiting sales to local consumers, producers are opening themselves up to a lot of potential price volatility, and to lower prices at the exact time they have produce ready to sell. How can the producers partially mitigate such effects? Find people in other locations with different seasons with whom to trade.

The authors write:

“It can be seen that local price premiums/discounts vary depending on product type and season. For grape and cherry tomatoes, there is an 18.18% local premium during season 1 (before the peak season). However, starting from season 2 (local peak season), price difference declines and becomes insignificant. On the other hand, there are constant local discounts for other tomatoes throughout the year, although prices are considerably lower in seasons 2 and 3. Comparing the results for both types of product, there is a clear downward effect on prices of local tomatoes during the peak production season, suggesting that market prices are likely influenced by the local production level.

One further contributing factor to the price discounting may be the capacity limitations in marketing and distribution by local producers in Hawaii. Since large national producers with more marketing and logistics competence have access to a larger market, production surpluses can be spread over more market areas with less need for discounting. In comparison, small local farms are often constrained by lack of distribution channels and market outlets (Martinez et al., 2010). In the case of Hawaii, because local tomatoes are exclusively supplied to the Hawaiian Islands, this may result in discounting at the retail level in times of production surplus.

Lastly, the Armington analysis shows that consumer choices with respect to locality and organic origins are elastic, and that both local and organic tomatoes are quite substitutable to import nonorganic tomatoes. ”