The April 2022 edition of our Consumer Food Insights report is now out.

A few highlights from this month:

The Sustainable Food Purchasing (SFP) index is up about 2 points since January

Consumer food spending fell slightly from March to April but remains about 9% higher than in January

Food insecurity rates are the lowest we’ve measured since the survey started

46% of consumers have heard of the recent bird flu outbreaks; 60% are concerned about the impact on food prices

This month, we did a deeper dive into differences in behavior of urban vs. rural consumers. Rural consumers are more likely to be food insecure and are less happy with their diets as compared to urban consumers.

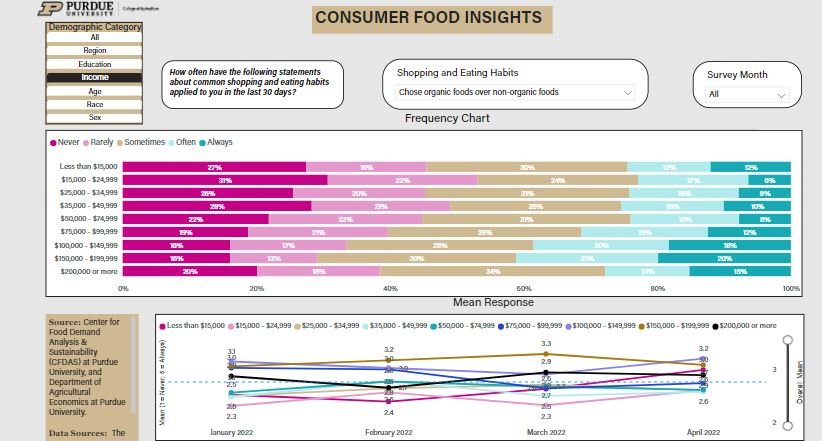

Finally, I’ll note that we’ve created our first data dashboard to explore current and past editions of the Consumer Food Insights survey. This dashboard focuses on the questions we ask about shopping and eating habits, and allows the user to see how these vary by demographic characteristics and by month of the survey. For example, the screenshot below shows propensity to buy organic food by income. Play around with the data yourself.

P.S. Kudos to Sam Polzin for his excellent work on the survey administration and reporting and to Anna Subramaniam for work on the data dashboards.