There seems to be a insatiable desire for information on regional food consumption patterns, fed by click-bait headlines fueled by dubious data sources. To help provide some “hard” data on this topic, about three years ago, I wrote a post about how meat demand varies by state. The graphs I presented then came from data collected from the Food Demand Survey (FooDS) we ran for five years, and they relate to measures of demand, not consumption.

I’ve been receiving a large number of emails in recent months about this post, which suggests even more demand for this type of information than I’d originally anticipated. Unfortunately, a big challenge is that there is no good, easily accessible, publicly available data on food consumption by U.S. state.*

Given the apparent interest in the topic, I turned to data collected by the Bureau of Labor Statistics (BLS) Consumer Expenditure Survey (CES). With special permission, one can access state-level consumer spending on food, but anyone can access their representative consumer spending data by U.S. census region. Here, I delve into that data to provide insights into how food spending varies by the nine Census regions they report.

First, here is data on total annual spending on food by region. Consumers in the Pacific Region (Alaska, California, Hawaii, Oregon, and Washington) spend the most on food at $9,166 annually in 2017-18, whereas consumers in the East, South Central Region (Alabama, Kentucky, Mississippi, and Tennessee) spend the least at $6,807/year.

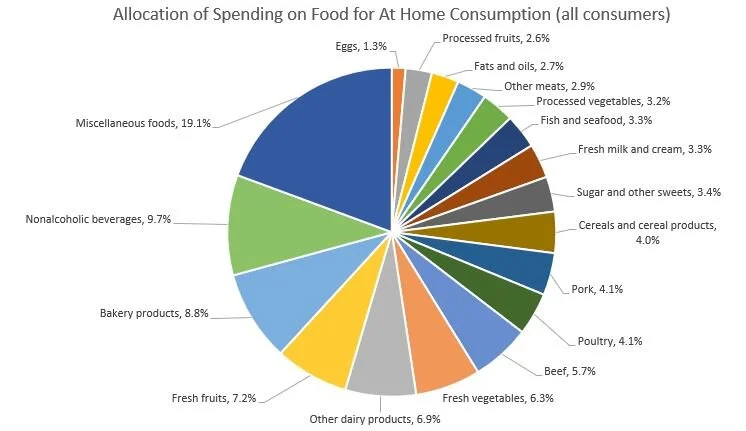

According to these data, on average about 43.6% of spending is on food to be consumed away from home (e.g., at restaurants), whereas 56.4% is spending for food to be consumed at home (e.g., spending at grocery stores). The BLS does not segregate data on spending on food away from home by the type of food, but it does so for spending on food to be consumed at home. Of the spending on food to be consumed at home (e.g., spending at grocery stores), the figure below shows the breakdown for the “average” food consumer. 19.1% of “at home” food spending is for “miscellaneous foods” and the next biggest category is nonalcoholic beverages (9.7%) and then bakery products (8.8%). Combined, all meat products including beef, pork, poultry, and fish account for 21.6% of at home food spending, and all dairy products account for another 10.2%.

The main reason for delving into these data is that they provide information on regional differences in food spending patterns. To explore these issues, I calculated the at food expenditure shares for each of the nine census regions, and then calculate the percent difference in expenditure share for a given region compared to the “average” consumer in the U.S. Here are some breakdowns, starting first with spending on beef as a share of all spending on food at home.

Differences in Spending on Beef by Region.

Consumers in the South West Central region (Arkansas, Louisiana, Oklahoma, and Texas) allocate 16.2% more of their at-home food budget to beef than does the national average food consumer, whereas on the other extreme, New England consumers (in Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, Vermont) allocate about 8.7% less of their food budget to beef than does the national average food consumer.

The following shows similar figures for pork and poultry. Whereas consumers in the Upper Midwest allocates a higher than average share of their food at home food budget to beef and pork, consumers there allocate 21.1% less of their food at home budget to poultry as compared to the average national food consumer.

Differences in Spending on Pork by Region

Differences in Spending on Poultry by Region.

Turning from meat items, here is data on relative spending on fresh fruits and fresh vegetables by region, which is higher in the West and New England.

Differences in Spending on Fresh Fruit by Region.

Differences in Spending on Fresh Vegetables by Region.

What about items that are often considered “unhealthy” like sugar and sweets and fats and oils? Spending on sugar and sweets is 27.3% higher in the Mountain region as compared to the average consumer, and spending on oils and fats is relatively highest in the East South Central Region.

Differences in Spending on Sugar and Sweets by Region.

Differences in Spending on Fats and Oils by Region.

The BLS CES reports spending on alcoholic beverages as a separate category from food at home or food away from home. Across all consumers, about 7% of food spending (either at home or away) is on alcoholic beverages. The variation across region is shown below. Spending on alcohol (as a share of total food spending) is positively correlated with spending on fresh fruits and fresh vegetables (as a share of spending on food at home), as alcohol spending is highest in the West and New England.

Differences in Spending on Alcohol by Region.

Finally, here is spending on food away from home as a share of total food spending. Consumers in the South West Central Region (Arkansas, Louisiana, Oklahoma, and Texas) and in the West spend 4% more on food away from home as a share of total food spending as compared to the average food consumer.

Differences in Spending on Food Away from Home by Region.

Readers who want to further explore the differences in regional spending patterns can access the BLS CES data here.

*The USDA Economic Research Service (ERS) reports data on per-capita “consumption” (this is actually “disapperance data, which infers consumption based on production, minus exports, plus imports, plus or minus net change in storage), but this is only at the national level. There are some other datasets which provide more local information on food purchases or consumption, but they are proprietary. Examples include grocery store scanner data by Nielsen or IRI. There are publicly available data, like the National Health and Nutrition Examination Survey (NHANES), which have information on location and food consumption, but it often requires significant data analytic abilities or special permission to make use of these data to explore state or regional trends.